AI Investing Can No Longer Rely on the "Models vs. Applications" Binary: Foresight Ventures' Five-Layer Investment Map

Executive Summary

Over the past two years, the most common framework used to think about AI investing has been the binary of "models vs. applications." It was a useful framework for a while. In the early phase of the AI cycle, model capability was genuinely the scarcest asset. Whoever could train the strongest model stood closest to the entry point, the developer ecosystem, enterprise budgets, and capital pricing.

But by 2026, the question itself has started to lose explanatory power.

AI is no longer just a software feature. It is becoming a full industrial system spanning power, chips, data centers, models, agent runtime, workflows, payments, identity, and service distribution. Many of the companies we see no longer operate in only one layer: the same company may sell chips and cloud, train models and provide tooling, run an exchange and also try to define the payment standard for agents. Meanwhile, the so-called application layer has begun to split from within. Vertical agents, harness middleware, agent-commerce protocols, and rollups of traditional services are, in substance, very different kinds of assets.

That is why Foresight Ventures believes AI investing needs to move beyond the "models vs. applications" binary and into a layered framework. What ultimately shapes returns is not simply whether a company sits in the model layer or the application layer, but what kind of moat it actually owns: physical scarcity, capital and talent oligopoly, execution-trajectory data, customer and workflow data, or network effects and standards lock-in.

NVIDIA's "AI five-layer cake," presented at GTC 2026, offers an important starting point. It breaks the AI industry into five layers: energy, chips, infrastructure, models, and applications. The value of that framework is that it reminds the market that AI is not a single-point software innovation, but an industrial-scale value chain. But this is still, at its core, a hardware company's perspective. It helps explain why NVIDIA can capture profit across layers, yet it does not directly answer the venture question of which layer to invest in.

Foresight's approach is to further split what NVIDIA compresses into one "application layer." We divide the AI investment stack into five layers: Physical Substrate, Frontier Intelligence, Harness, Workflow Ownership, and Agent Commerce + Identity.

Each of these five layers corresponds to a different investment question. Physical Substrate is about capex and physical bottlenecks. Frontier Intelligence is about capital, talent, and model oligopoly. Harness is about whether execution trajectories can be accumulated and structured. Workflow Ownership is about who owns the customer, the process, and the outcome data. Agent Commerce + Identity is about payments, identity, service discovery, and standards networks.

Our core view is this: the AI application layer should not be judged merely by whether it "has an agent." What matters far more is whether it truly owns the workflow. The most valuable AI companies of the next cycle may not be the ones with the flashiest interface or the smartest demo. They will be the ones that enter real businesses, control the execution chain, accumulate outcome data, and turn AI transformation into better unit economics.

This is also where the crypto and exchange opportunity sits. Agent commerce, identity, payments, settlement, and service discovery will become part of the economic substrate of the agent economy. But the core standards positions are being captured quickly by players such as Coinbase, Cloudflare, Stripe, Visa, Google, and Anthropic. For Foresight and Bitget, the more realistic opportunity is not to rebuild a peer protocol from scratch, but to secure early positions in cross-rail settlement, KYA, agent identity, trading-execution harnesses, and high-value financial workflows.

Why "Models vs. Applications" Is Starting to Break Down

At the start of the AI cycle, it made sense for the market to focus on models. Without sufficiently capable foundation models, there would be no coding agents, AI customer support, AI search, agentic workflows, or automated trading. The model layer set the ceiling of capability, and it also explains why companies such as OpenAI, Anthropic, Google DeepMind, and xAI captured the highest valuations and the most concentrated pools of capital.

But once model capability began to diffuse, the investment question changed. What enterprises actually care about is no longer just whether a model can answer a question. They care whether it can plug into internal systems, obtain the right permissions, run reliably over long tasks, remain accountable when something fails, expose the execution process for inspection, measure outcomes, and improve after errors.

Those are no longer model questions. They belong to production environments, workflows, permissions, payments, risk controls, auditability, and data feedback loops.

That means the AI value chain is expanding from "who has the best model" to "who can turn intelligence into real execution."

This is where the old "models vs. applications" binary becomes too coarse. What gets grouped into the "application layer" now contains at least three entirely different opportunity sets. The first is Harness: memory, tool calling, orchestration, evaluation, tracing, and guardrails. The second is Workflow Ownership: concrete business processes in customer service, legal, accounting, insurance, recruiting, financial research, and more. The third is Agent Commerce + Identity: how agents discover services, call services, pay, authenticate, and establish trust with each other.

All three may look like "applications," but their moats, customers, business models, and exit paths are fundamentally different. Underwriting them in one bucket is an easy way to get the thesis wrong.

So Foresight is no longer asking "models or applications?" The real question is: which layer of the AI value chain does this project occupy? Where does the moat in that layer come from? Does it own some durable barrier based on data, workflow, network effects, or physical scarcity?

From NVIDIA's Hardware Five Layers to Foresight's Venture Five Layers

NVIDIA's "AI five-layer cake" divides the AI system into five layers: energy, chips, infrastructure, models, and applications. Its greatest contribution is to move AI back out of the narrow software frame and into an industrial-systems frame.

From NVIDIA's perspective, the first three layers together form the AI Factory. Power, chips, data centers, networking, cooling, and cloud infrastructure collectively determine the productive capacity of the AI era. The more prosperous models and applications become, the stronger the demand for the underlying AI Factory. NVIDIA's real strength is not just that it sells GPUs. It acts across layers - chips, networking, CUDA, NIM, DGX Cloud, robotics, autonomous driving - to keep as much of the value chain as possible anchored around its strongest position.

But a venture fund cannot simply copy NVIDIA's perspective. NVIDIA cares about which layers pull GPU demand forward and which layers reinforce its own platform control. Venture investors care about different questions: which layers can still produce new companies, which ones have sustainable moats, which ones remain investable at sensible prices, and which ones offer clear exit paths.

That is why Foresight reconstructs the AI investment stack into five layers.

| Layer | Name | Moat Type | One-line Investment Logic |

|---|---|---|---|

| 1 | Physical Substrate | capex + physical scarcity | Back the load-bearing pillars of AI demand, not direct combat in the silicon wars |

| 2 | Frontier Intelligence | capital + talent oligopoly | The general-model oligopoly is largely set; be selective around Physical AI and World Models |

| 3 | Harness | trajectory data | Standalone middleware is losing independence; focus on vertical integration or M&A optionality |

| 4 | Workflow Ownership | customer + workflow data | Focus on who owns the customer, the process, and the outcome data, and whether pricing can move to per-outcome |

| 5 | Agent Commerce + Identity | network economics + standards lock-in | Standards competition is heating up; watch connectors, identity, and cross-rail settlement |

The point of this framework is not classification for its own sake. It is a reminder that every layer requires a different due-diligence method. Physical Substrate requires analysis of capacity, orders, PPAs, power costs, and geopolitical risk. Frontier Intelligence requires judgment on talent density, capital intensity, and data flywheels. Harness requires analysis of execution trajectories and the optionality of strategic acquisition. Workflow Ownership requires evaluation of customers, processes, gross-margin improvement, and outcome-based pricing. Agent Commerce requires attention to protocol adoption, standards lock-in, and cross-organization call volume.

Layer 1: Physical Substrate - Back the Load-Bearing Pillars of AI Demand

Physical Substrate is the physical base layer of AI: chips, packaging, memory, networking, optical communications, power, cooling, data centers, and neocloud.

This layer looks much closer to traditional semiconductor, energy, and industrial research than to software investing. It does not speak through demos. It speaks through capacity, orders, capex cycles, gross margins, customer concentration, supply chains, and geopolitical exposure.

Our judgment here is straightforward: the most compelling areas are not independent AI-chip startups, but power, cooling, networking, packaging, and leading neocloud players.

The most important new variable is how agent workflows amplify underlying infrastructure load. Agents are not simply replacing "one question-answer interaction" with "one more expensive interaction." They turn interaction into a long-running, multi-step, multi-model, multi-retry execution chain. A single agent task may include planning, retrieval, tool use, code execution, failure retries, permission confirmation, and result verification.

That means we cannot extrapolate demand in the agent era from ChatGPT API-call curves alone. What actually drives infrastructure demand is agent step count, retry rate, and tool-call density. Those variables amplify compute, memory, networking, and observability all at once.

The window for independent silicon startups is also narrowing. NVIDIA, AMD, Google TPU, AWS Trainium, and Microsoft MAIA have already established a formidable landscape. A chip startup whose entire pitch is "cheaper or faster than NVIDIA" has to overcome financing risk, software-ecosystem risk, customer-migration risk, and mass-production risk at the same time. That is a very difficult underwrite.

By contrast, power and cooling look more like hard bottlenecks in the AI capex cycle. Even if model prices fall and inference efficiency improves, data-center demand for power, heat dissipation, transformers, power distribution, and construction lead time does not disappear. Expansion of the AI factory turns compute competition, at its core, into an energy and infrastructure competition.

Neocloud sits in a gray zone between the public and private markets. Companies such as CoreWeave, Nebius, Crusoe, and GMI Cloud benefit from GPU demand, outsourced AI workloads, and supply gaps outside the major cloud providers. But they also carry high customer concentration, heavy capital intensity, and cyclicality risk when supply-demand conditions reverse.

There is another valuation shift here that LPs should notice. Historically, memory, networking, optical-module, and equipment companies were often priced on price-to-book, inventory cycles, and pricing inflection points. But if agentic workloads structurally amplify demand, the valuation anchor for assets such as Micron, Arista, Coherent, and Lumentum may begin to migrate from PB toward PEG. Investors will ask less, "how far does this cycle run?" and more, "can agent workload sustain a steeper demand curve over the next three to five years?"

NVIDIA's own narrative will also evolve. The first bull case was GPU scarcity. The next and harder question is whether GPUs, memory, networking, and storage can be orchestrated efficiently enough for larger and more complex agentic workloads. The real bottleneck is no longer just whether GPUs exist, but whether the entire AI factory can achieve high utilization, throughput, and low unit-token cost.

Foresight's stance on this layer is: it is investable, but it should not be venture's main battlefield. It is better approached through public markets, pre-IPO opportunities, structured deals, or participation in category leaders. Key diligence items include order visibility, locked-in power pricing and PPA structure, unit economics per MW, customer concentration, depreciation cycles of equipment, and geopolitical and supply-chain exposure. The key disconfirming signal is also clear: if hyperscaler capex utilization falls materially while agent demand fails to absorb new supply, the growth re-rating of Physical Substrate assets needs to be revisited.

Layer 2: Frontier Intelligence - The General-Model Oligopoly Is Set, but Physical AI Still Has a Window

Frontier Intelligence is the capability layer of AI models: general text models, multimodal models, video and audio models, code models, world models, robotics models, and bio frontiers.

The defining characteristic of this layer is capital and talent oligopoly. The strongest models require the strongest researchers, the largest compute budgets, the strongest data flywheels, and the deepest distribution channels. General models are no longer a market that an ordinary early-stage VC can underwrite effectively.

Our view is that the general-model layer has entered an oligopoly phase. Incremental alpha is no longer in small-model startups, but in sub-layers that are still unsettled - especially Physical AI and World Models.

The structure of the text frontier is already clear. OpenAI, Anthropic, Google DeepMind, xAI, Meta, and a small number of leading Chinese model companies control most of the capital, users, developers, and enterprise entry points. A new independent small-model startup may still lead on some benchmark, but it is increasingly hard for that advantage to compound into a durable standalone company.

Code models are also being absorbed rapidly by the oligopoly. Claude Code, the GPT family, Gemini, Cursor, Devin, and related products are collapsing coding-model capability and coding-agent workflow into one stack. That leaves less room for an independent coding-model category.

Physical AI and World Models are still earlier. They require not just models, but embodiment, real-world data, sim-to-real capability, hardware supply chains, task coverage, and deployment environments. The data flywheels around robotics, autonomous driving, industrial automation, and embodied intelligence are not yet fully settled.

That is why companies such as Physical Intelligence, Wayve, Waabi, Skild AI, Figure AI, 1X Technologies, and Sanctuary AI remain worth tracking closely.

But this layer also cannot be approached with broad, undifferentiated optimism. The real diligence questions are concrete: how many real embodied systems are deployed, whether task coverage is high-frequency enough, whether the sim-to-real gap is narrowing, whether the data comes from the real world or from simulation, whether commercialization should begin in enterprise and industrial environments or go directly to the consumer home, and whether unit economics can work before hardware costs compress meaningfully.

Foresight's stance on this layer is selective participation in Physical AI while refusing to chase general-model narratives at elevated prices.

Layer 3: Harness - The Harness Is the Dataset

Harness is the execution system that brings models into production. It includes memory, context, tool calling, skills, orchestration, guardrails, evaluation, tracing, and observability.

If models provide intelligence, Harness provides executability.

Over the past year, the market has produced a long list of agent middleware: memory tools, tool-calling platforms, orchestration frameworks, observability products, evaluation platforms, and safety guardrails. They all solve real problems. But from an investment perspective, the independence of standalone middleware is declining.

That pressure comes from two directions.

On one side, model companies are turning tool calling, computer use, skills, memory, evaluation, and agent builders into native capabilities. OpenAI, Anthropic, Google, and Microsoft are unlikely to leave the core agent runtime to third parties indefinitely.

On the other side, vertical agent companies that truly own the customer and the workflow will internalize key parts of the harness themselves. Customer-support agents, legal agents, trading agents, insurance agents, and accounting agents will not permanently outsource their most valuable execution trajectories, customer data, evaluation standards, and risk logic to a generic middleware vendor.

So the real opportunity in Harness is not "another point solution," but two more durable shapes.

The first is the vertically integrated harness for specific high-risk industries. Financial services, trading, insurance, legal, and healthcare need context, tools, permissions, guardrails, tracing, evaluation, and feedback loops fused into one full-stack system. The moat here comes from the closed loop, not from any individual module.

The second is infrastructure that exits through strategic acquisition. Large security vendors, cloud companies, data platforms, and model providers will keep acquiring companies in evaluation, observability, guardrails, AI security, and workflow runtime. Harness middleware may never become the next independent platform giant, but it can still become a valuable strategic asset.

The most important sentence in this layer is: the harness is the dataset.

What matters is not raw logs. What matters is execution trajectory data that captures context, tool calls, decision process, failure modes, outcome attribution, and human feedback. Whoever captures high-quality execution trajectories is the one most likely to own the next wave of model training, agent improvement, and workflow-automation data assets.

Key diligence questions include whether the company captures real execution trajectories, whether those trajectories are stored in a structured schema, whether it has the user authorization and compliance boundary needed to retain that data, whether the product remains model-agnostic across providers, whether it has optionality to be acquired by a platform or a vertical operator, and whether it has entered high-value workflows rather than only demo infrastructure.

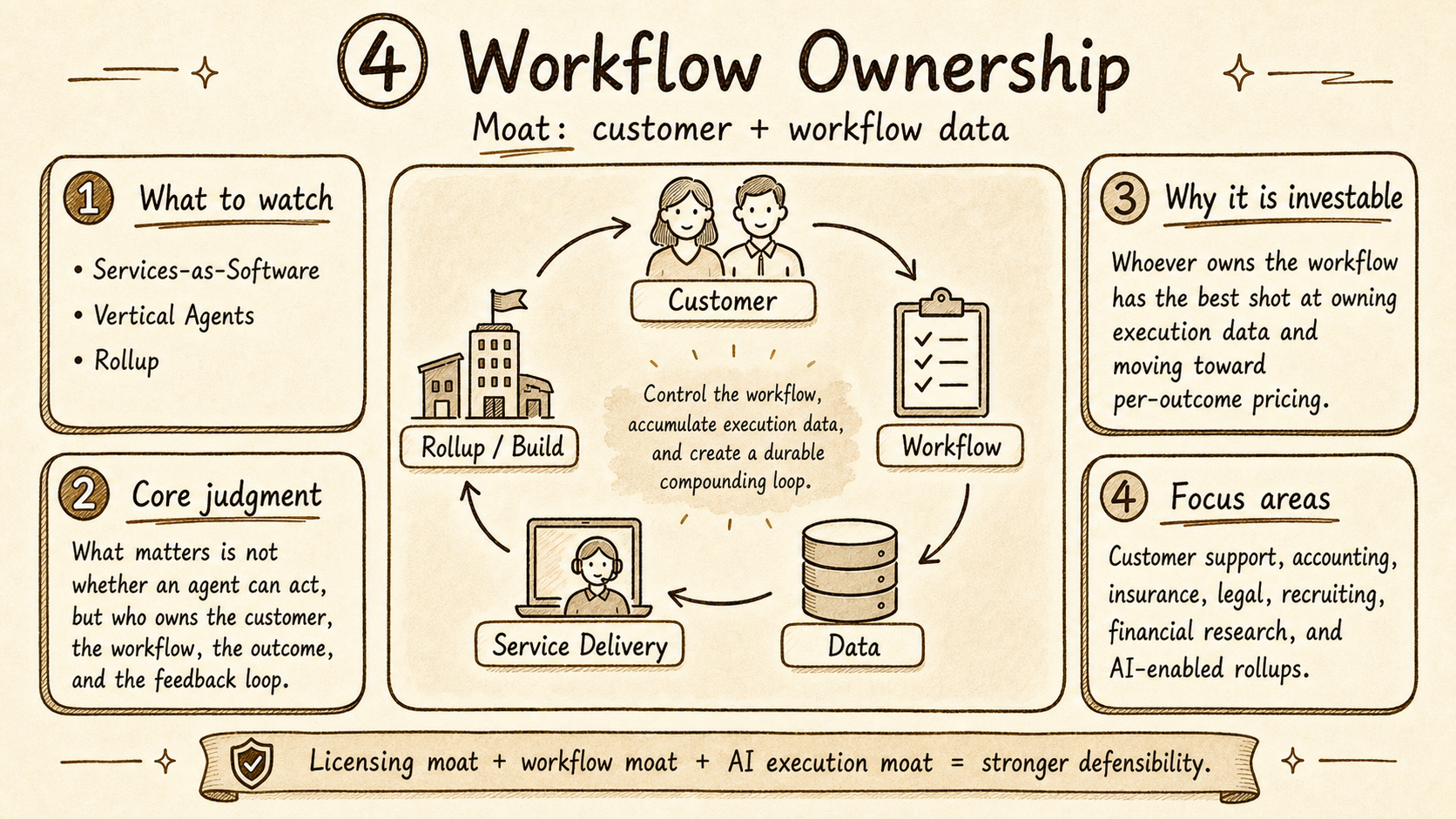

Layer 4: Workflow Ownership - The Real Question Is Who Owns the Workflow

Workflow Ownership is the part of the AI application layer that deserves the most careful differentiation.

The reason is simple: whoever owns the workflow owns the execution data; whoever owns the execution data has the best chance of achieving outcome-based pricing.

The default model in the SaaS era was to sell tools into a business. The stronger model in the AI era may be to embed much more deeply into the business process - or even to operate the business itself.

Traditional SaaS improves customer efficiency, but the customer still owns the process, the staff, the data, and the result. If an AI company only sells a tool, it often cannot access full execution data or truly charge based on outcomes. It remains limited to subscriptions, seats, or usage pricing.

But once an AI company enters the business itself and owns the customer, the workflow, the people, the execution result, and the feedback data, it stops being a tool vendor and starts becoming a new kind of service operator. It can transform low-margin, labor-intensive, repetitive service sectors into AI-native operating companies.

The essence of Workflow Ownership is not whether an agent can complete a task in isolation. The real question is whether the company owns the customer, the process, the outcome, and the feedback loop around that task chain.

Anthropic's recent launch of an enterprise AI services firm with Blackstone, Hellman & Friedman, and Goldman Sachs is a strong signal of this trend. The commercialization path of frontier-model companies is evolving from "selling tokens and APIs" toward "selling organizational capability": embedding Claude, engineering teams, and industry know-how directly into customer workflows in order to rewrite core enterprise processes. This looks closer to Palantir-style forward-deployed engineering than to traditional software distribution.

The investment implication is significant. Model APIs themselves will gradually commoditize, and both gross margin and pricing power will come under pressure. But token-embedded workflows are different. They embed model capability into customer processes, permissions, data, delivery, and outcome measurement, creating much stickier surfaces and stronger pricing power. The real alpha of frontier companies may come not only from model performance, but from vertical integration into Workflow Ownership.

How to Invest in Workflow Ownership

This layer cannot be judged on product demos alone. A vertical agent that appears able to automate a task does not automatically have a long-term moat. Four questions matter much more.

First, does it own the customer relationship? If the AI company is only a tool sitting on top of the customer's internal systems, then the relationship and the data remain with the incumbent enterprise. That still looks like SaaS. If it delivers outcomes directly to the end customer, or becomes deeply bound to the customer's core process, it looks much more like a workflow owner.

Second, does it own the full execution chain? Advice, drafting, summarization, and information retrieval alone are limited sources of value. A company that can create a closed loop from task intake to execution, exception handling, result delivery, and postmortem feedback is the one most likely to accumulate durable execution data.

Third, does it own measurable outcomes? Workflow Ownership works best in domains where results can be quantified: customer-support resolution rate, insurance loss ratio, accounting delivery efficiency, legal-review accuracy, recruiting match success, sales conversion, or trading-execution quality. If outcomes cannot be measured, outcome-based pricing becomes difficult.

Fourth, can the AI transformation show up directly in unit economics? AI is not just about adding an assistant to the product. It should reduce delivery cost, improve gross margin, shorten delivery cycles, and raise revenue or output per employee. Eventually it must show up in gross margin, EBITDA, retention, expansion, and pricing power.

Why Rollups Matter

Vertical agents may be one of the biggest application opportunities of the AI era, but the best vehicle may not always be a traditional software startup. One especially important path is the rollup model: acquire traditional service businesses, take control of the customers and workflow, then use AI to rebuild delivery.

The advantages are easy to see. If you sell tools to an accounting firm, an insurer, or a BPO, the data rights usually stay with the client. Once you acquire and operate the business itself, the AI company directly owns the process, historical cases, employee operations, customer feedback, and outcome data. Traditional SaaS can rarely charge per ticket resolved, per audit completed, per risk underwritten, or per claim processed, because it is not responsible for the final outcome. After a rollup, the company runs the business directly and can much more credibly move from software subscriptions to per-outcome revenue.

AI transformation also appears directly in gross margin. Traditional service sectors often have low gross margin, heavy labor dependence, and fragmented processes. If AI can replace a large share of repetitive work, the improvement shows up not as a product metric but as EBITDA and margin expansion.

There is also a moat that the market often underestimates: licenses and regulatory assets. If an AI-native company only sells a tool, it can be caught by traditional service firms or by model companies moving downstream. But if it also owns licenses, customer relationships, compliance capability, and the execution system, defensibility becomes much stronger. Corgi's acquisition of a full insurance-carrier license and Crete's control of multiple accounting-partner platforms are not just "software plus services." They are composite structures made of regulatory moat, workflow moat, and AI execution moat.

Crete Professionals Alliance, Corgi, and Crescendo + PartnerHero all suggest the same thing: AI is not simply upgrading SaaS into smarter software. In some industries it is breaking the boundary between software companies and service companies altogether.

There is also a lighter-weight route: instead of running the rollup directly, sell tools into PE-backed rollups. Many traditional private-equity rollups already control dozens or even hundreds of locations, have unified financial oversight, and have a clear mandate for margin improvement. What they lack is AI workflow tooling that can be plugged in quickly. For startups, that can be a faster path than cold-starting one industry customer at a time. For investors, these companies are effectively serving the rollup ecosystem, not generic SaaS demand.

Which Workflow Ownership Opportunities Are Worth Watching

The more attractive Workflow Ownership opportunities usually share several characteristics: high-frequency processes, labor intensity, measurable outcomes, customers willing to pay for results, enough industry fragmentation, and clear room for AI to improve delivery cost.

Customer support and BPO are the most intuitive examples because resolution rate, response time, and customer satisfaction can all be measured. Accounting and tax are also compelling because the processes are standardized, the deliverables are clear, and the market includes many small and mid-sized operators. Insurance and claims are attractive because they are both data-intensive and rules-intensive, with a tight linkage between risk pricing and outcome. Legal and compliance are document-heavy, process-complex, and expensive to get wrong. Recruiting and sales are trackable, but they can easily fall into tool commoditization unless they control real distribution and customer data. Financial research and trading execution offer the clearest outcomes, but they also impose the highest demands on compliance, permissions, and risk control.

The companies to treat cautiously are vertical agents that have only UI and prompt workflow, but no customer data and no outcome loop. They may look like applications, but they are often only short-term packaging around model capability. AI tools sold purely for internal enterprise use, without access to execution data, can still become good SaaS businesses, but they do not necessarily own the workflow. Embedded AI that relies too heavily on model differentiation will also be squeezed as model companies ship native features. And the rollup narrative itself should not be romanticized. Without M&A capability, financial integration, process redesign, AI implementation, and real industry operating ability, an AI rollup can quickly become nothing more than a traditional PE rollup with a layer of automation marketing on top.

So the investment question in Workflow Ownership is not "is this a vertical agent?" The right question is: does it truly own the workflow, does it own the outcome, and can it turn AI transformation into better unit economics?

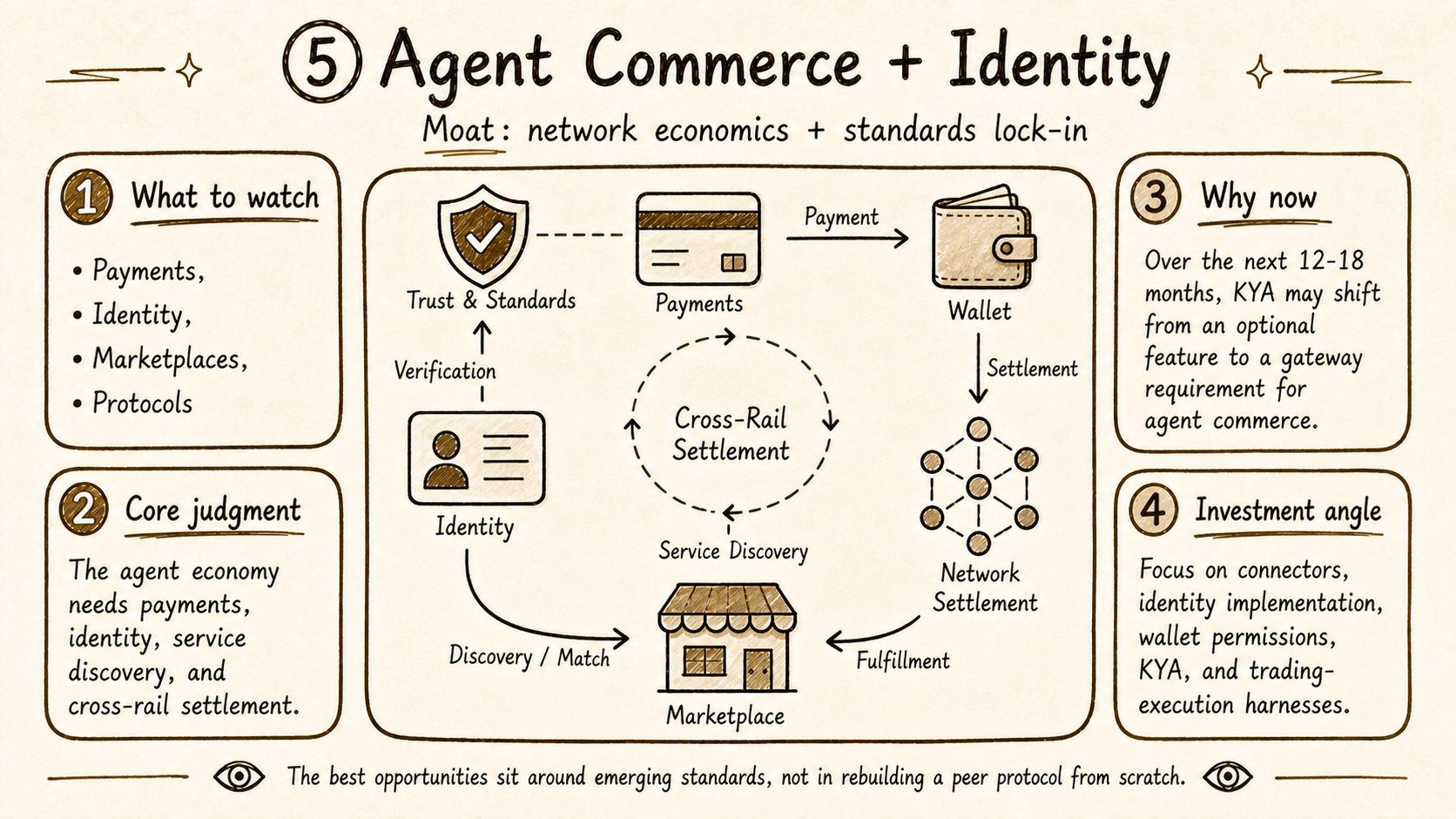

Layer 5: Agent Commerce + Identity - Crypto's Real Opportunity Is in Payments, Identity, and Execution Networks

Agent Commerce + Identity is the most natural intersection between AI and crypto.

Agents need to discover each other's services, call those services, verify identity, obtain permissions, pay for usage, complete settlement, and leave an auditable record. These are precisely the kinds of problems crypto and open-finance systems have spent the last decade trying to solve: digital identity, programmable payments, stablecoin settlement, open protocols, wallet permissions, and verifiable on-chain records.

But that does not mean every AI x crypto project is worth funding. Most "AI tokens" and "agent tokens" are still narrative assets rather than real commerce infrastructure. The truly valuable layers are the parts of the agent economy that look like infrastructure: payment rails, identity and reputation, service discovery and marketplaces, protocols, and developer standards.

The challenge is that the key standards positions are being occupied very quickly by large platforms.

The area that deserves the highest near-term priority is KYA, or Know Your Agent. In financial services, payments, trading, and enterprise systems, non-human identity density is rising quickly. Agents, bots, service accounts, API clients, and automated workflows will soon outnumber human employees by a wide margin. Over the next 12 to 18 months, agent identity may shift from an optional security feature to a basic entry requirement for agent commerce.

KYA is not about assigning a static identifier to an agent. It is about answering four questions: whom does this agent represent, what is it authorized to do, where are the permission boundaries, and who is accountable when something goes wrong? Without that foundation of identity and responsibility, agent payments, agent marketplaces, machine-to-machine transactions, and automated trading all run into a trust bottleneck.

MCP has already become one of the de facto standards for connecting agents to tools and external systems. A2A is pushing cross-framework communication between agents. x402 and Agentic.Market signal Coinbase's ambition to define standards in agent commerce. Stripe, Visa, and PayPal will not give up the fiat-side entry point into agent payments either.

So Foresight's strategy is not to rebuild another x402 or another A2A at the same layer. The better hunting ground is the set of still-unlocked positions around those standards. That includes connectors for cross-chain, cross-fiat, and stablecoin settlement; implementation layers for agent identity and KYA; wallet permissions, session keys, and delegated payments; vertical entry points into agent-service marketplaces; execution and risk-control harnesses for trading agents; and enterprise layers for audit, permissions, compliance, and risk management.

For Bitget, this layer matters especially. Exchanges and wallets naturally sit on the funding and execution paths of agent commerce. If future agents trade on behalf of users, pay for services, subscribe to data, buy services, allocate into RWA, or settle across borders, competition between platforms will not be decided only by "who has more users." It will also be decided by "who becomes the default account, liquidity, and settlement layer that agents call."

That is why exchanges should not stop at building an AI chatbot. They should be building agent-native accounts, permission systems, execution traces, risk controls, KYA capabilities, and settlement infrastructure.

A Cross-Sectional Validation Through Y Combinator Startups

The five-layer framework is not only theoretical. YC W26 offers a useful cross-sectional validation: the center of gravity in AI startups is clearly shifting from "build a copilot tool" toward "replace or own a specific workflow."

Public Demo Day observations suggest that among roughly 199 YC W26 companies, AI-native products made up a very large share, B2B remained the dominant orientation, and hardware, robotics, industrial, and defense-related projects came back strongly. More importantly, many companies no longer describe themselves in the language of copilots. They now explicitly emphasize replacing human workflow, AI-native services, "Claude Code for X," vertical automation, and outcome-based delivery.

That lines up almost perfectly with the conclusions of the five-layer framework.

Workflow Ownership is both the most crowded and the most natural landing zone for startups. Customer support, legal, recruiting, accounting, insurance, financial research, construction, engineering, DevOps, QA, healthcare, hotel front desk, aircraft maintenance, ranch operations, fish farming, and grid planning are all answering the same question: can AI take over a specific workflow and convert delivery from labor-intensive service into software-like service production?

Harness is still necessary, but dangerous. The YC sample also includes agent infrastructure, runtime, guardrails, observability, and financial infrastructure projects, but this layer will separate quickly. Generic agent infrastructure without unique trajectory data, without access to high-value workflows, and without a path to acquisition by model companies or vertical operators is highly vulnerable to compression by native platform features.

Agent Commerce remains surprisingly under-supplied on the startup side. That is not because it is unimportant, but because its key variables are not ordinary product-market fit. They are network effects, standards lock-in, and cross-organization adoption. Payments, identity, service discovery, and agent marketplaces are more likely to be pushed forward by platform players such as Coinbase, Stripe, Visa, Anthropic, Google, and Cloudflare. Startup opportunities are more likely to sit in connectors, identity implementation, wallet permissions, and vertical-market entry points.

The PE rollup channel is also evolving from a side topic into a real investment lead. Some YC companies are no longer trying to sell directly to one SMB at a time. They have realized that PE-backed rollups are a more efficient distribution path: one PE relationship can open dozens or even hundreds of operating locations, and AI tooling can be tied directly to margin improvement. This validates the central claim of Workflow Ownership: the valuable asset is not the tool itself, but the fact that the tool has entered a workflow network that has already been consolidated.

Defense and national security are also entering venture focus again. Counter-drone systems, military unmanned systems, specialty equipment, and government-contract AI projects are starting to show real order flow. These opportunities do not sit neatly inside the five-layer framework, because their moat comes less from software data flywheels and more from government relationships, long contract cycles, procurement access, and defense-industrial positioning. They should be tracked as a separate watchlist rather than forced into the AI application bucket.

The significance of YC W26 is not that every vertical agent deserves funding. It is that it confirms a much larger structural shift: the main battlefield of AI entrepreneurship is moving from "give people a better tool" to "deliver a concrete business outcome for them." That is exactly the investment premise behind Workflow Ownership.

Foresight's Allocation View: Own Fewer Generic AI Bets, More Ownable Workflows

Based on the five-layer framework, we suggest adding one unifying diligence formula: output per unit of token spend.

The market used to focus on token call volume, API usage, user activity, and agent execution counts. But in the next phase, the real question is: for every dollar of model cost, how much revenue is created, how many labor hours are saved, how many errors are prevented, how much conversion is improved, or how much risk loss is reduced?

Put differently, investors should not stop at asking "how many tokens does this product use?" They should ask:

Output per unit token = revenue uplift / cost savings / error reduction / risk reduction divided by model and execution cost

This formula is especially useful for Workflow Ownership. If a downstream AI product cannot present a clear outcome metric, it is highly likely to be removed in an enterprise budget audit within 12 months. The resilient companies will be the ones that can prove AI spend converts into measurable business outcomes rather than "employees like using it."

From an allocation perspective, Foresight's strategy can be summarized in five points.

First, in Physical Substrate, back the load-bearing pillars, not the silicon wars. Power, cooling, packaging, networking, and leading neocloud players deserve sustained attention, but early hardware startups should not be Foresight's main battlefield.

Second, in Frontier Intelligence, do not chase general-model narratives. Be selective around Physical AI and World Models. General models are already in oligopoly territory; the less-settled openings remain embodied intelligence, robotics, world models, and a small number of bio-frontier opportunities.

Third, in Harness, avoid generic middleware and back vertical closed loops or strategic-acquisition optionality. Point solutions in memory, tool calling, evaluation, and tracing are easy to absorb into model platforms or to internalize within vertical agents. The real value lies in complete harness systems inside high-value workflows.

Fourth, in Workflow Ownership, focus hard on ownership. Pay special attention to AI-enabled rollups, services-as-software, and companies that own the customer, the process, the data, and the outcome. The strongest opportunities are not just about helping an enterprise become more efficient; they are about owning the business and then rebuilding it.

Fifth, Agent Commerce + Identity is the strategic positioning layer for Foresight and Bitget. Do not get distracted by vague AI-token narratives. Focus on payments, identity, permissions, service discovery, cross-rail settlement, and agent-native accounts.

If the entire strategy must be reduced to one sentence, it is this: the next phase of AI investing is not about backing a smarter demo. It is about backing companies that own the execution chain, the data loop, and the standards surface.

Conclusion: The AI Value Chain Is Being Reallocated

The first phase of AI belonged to models. The second phase belongs to the companies that can turn models into real execution systems. The third phase will belong to the companies that own workflows, data loops, and standards networks.

The "models vs. applications" binary cannot see that third phase clearly.

The real questions are these: who owns the physical bottlenecks, who controls frontier intelligence, who accumulates execution trajectories, who owns the customer and the workflow, and who defines the standards of agent commerce and identity?

Foresight's five-layer framework exists to separate those questions cleanly.

Our most important conclusion is this: the biggest venture opportunities in the next AI cycle are not likely to sit in bottom-layer general models, nor in top-layer AI wrappers. They will sit in the companies that can own high-value workflows. These companies may not look like traditional SaaS firms at all. Some may look more like PE rollups, BPOs, insurers, accounting firms, trading-execution platforms, or payment networks. But precisely because they enter real business operations, they have the chance to own execution data, outcome data, and long-duration compoundable moats.

For Foresight and Bitget, this is not only a financial-investment view. It is also a strategic route. In the agent economy, trading, payments, identity, asset distribution, and execution networks will all be redefined. The goal is not to repeat that "AI matters." The goal is to back the layers that can genuinely reshape financial entry points, execution chains, and the way capital is formed.

The next wave of AI alpha will not come from repeating "the model is strong" or "applications are exploding."

It will come from asking a more precise question: which layer does this company really own, is the moat in that layer real, and can repeated execution be turned into a data asset that makes the next execution better?